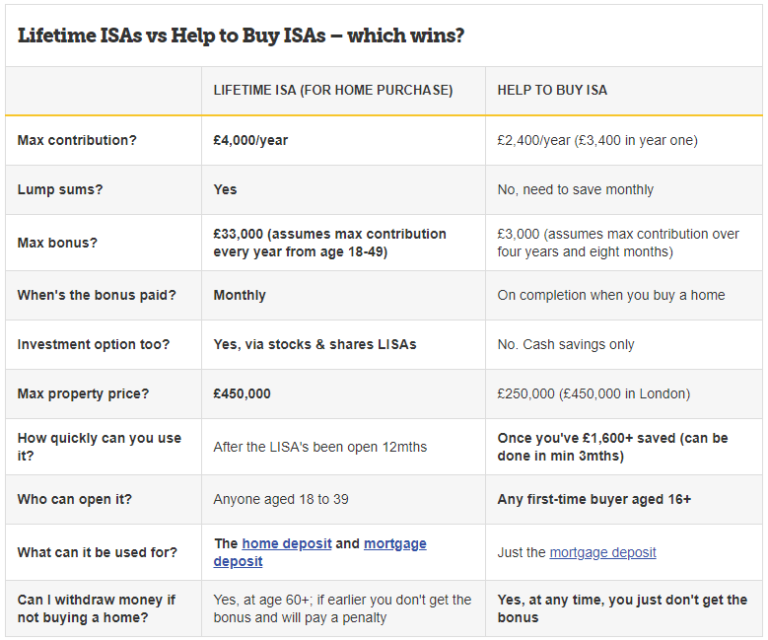

So with this in mind, two years ago I opened up a Help to Buy ISA, set up a direct deposit for £200 every month and left it to do its thing. I knew I wouldn’t be buying a property anytime soon, but I also knew the earlier I started paying money in, the bigger the opportunity was for my 25% bonus to grow into a larger amount of money before I needed to buy a property.

Now, when buying a house, people tend to put down a deposit which is between 5-10% of the value of the property. A £400,000 property would require a deposit of £20-40k for example. One of the biggest challenges that people face when buying a property is raising the funds to cover this initial deposit. A recent article I read in the FT (link here) stated that:

‘Two-fifths of 18 to 40-year-olds’ have saved nothing towards their first home’

This is shocking – 40% of us have no savings??

‘The average pot saved towards a deposit among other respondents was £8,300, with men saving an average £11,600 and women £5,620. When asked what they were targeting as a total saving for a deposit, participants’ responses averaged £24,816 — significantly below the average deposit of £44,000 put down by first-time buyers in figures published in March by the Office for National Statistics.’