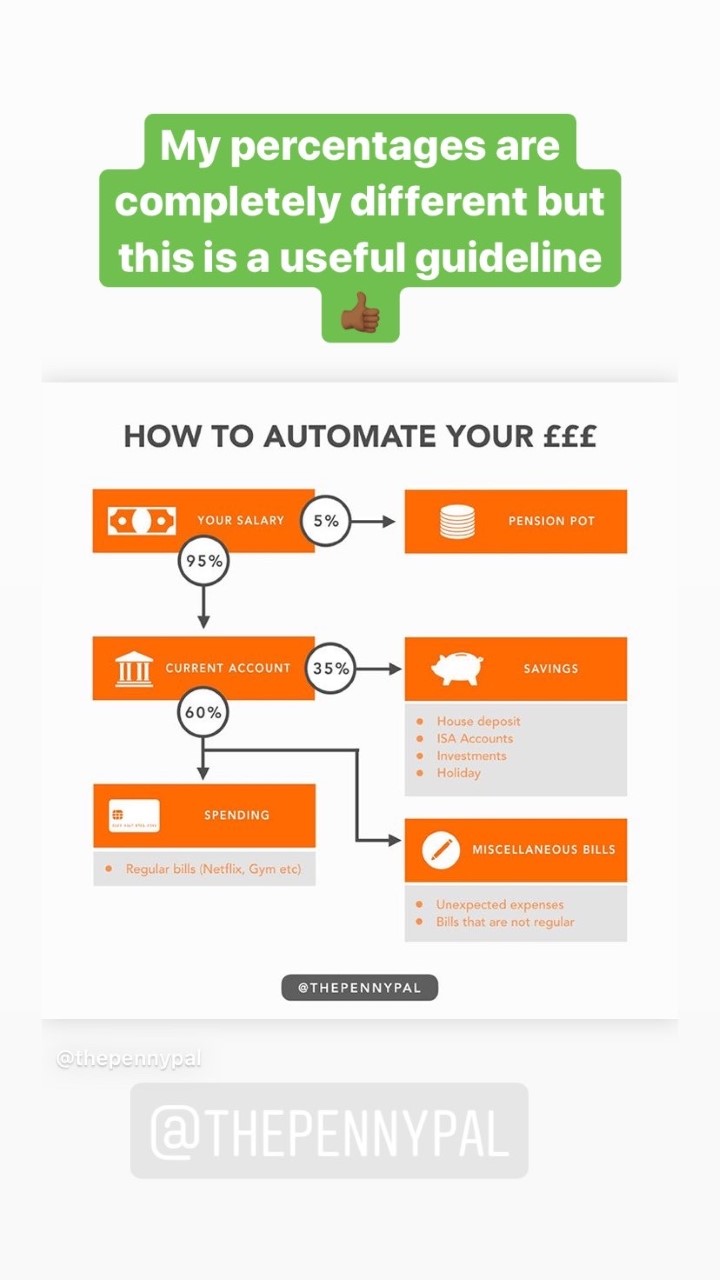

As you can see, the responses ranged from full agreement to outright scepticism, which is absolutely justified. When browsing through the internet there are various financial gurus that have their own take on how much you should be saving etc. The 50/30/20 rule says that you should, ‘reserve 50 percent of your budget for essentials like rent and food, 30 percent for discretionary spending, and at least 20 percent for savings’. There’s also the 70/20/10 rule for living expenses, savings and paying off debt respectively. Everyone is different but, as I’ve said before, most of the people that read this blog are under the age of 35 and are consequently young enough to invest more of their money and should be doing so. The older you get, the less time you have to take advantage of compounding (which is when your investments grow to produce very high returns over a long period of time) so the earlier you can get started, the better.

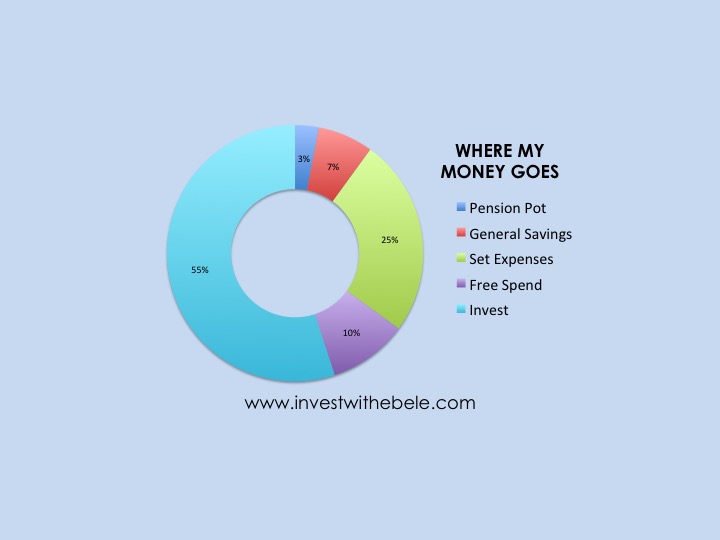

Having that in mind, I think it may be helpful to share what my breakdown is. If I was to create my own diagram a la @thepennypal, it would look something like this: