2021 Investment Portfolio Performance Review

An investment portfolio is just a way of describing all the things I have invested in to make more money. Today I will be going through just how much my portfolio has grown over the last 12 months to see how much return I have made. This is the first time I have done this.

Why am I doing this review?

Well I think with anything worth doing you should be able to track how well (or badly) it has done. If I was on a weight loss journey, I would track my start and end weight to see progress. If I was practising for a 100m sprint I would monitor my race time and aim to improve. I also think it will be exciting to look back on this in 10/20 years and see how the choices I make now impact my future. And most importantly, I made an Instagram poll and 98% of respondents wanted to know how my portfolio fared in 2021, so here we are.

Now, before I get into it there are some caveats that I will outline. Firstly, there are so many methods of calculating investment performance. Time weighted return, money weighted return etc all take into account varying factors, but I don’t want to overcomplicate things – I could include lots of fancy equations and then you would all get bored and no one would make it to the end of this post. For the sake of simplicity, I am calculating returns as the invested amount vs the final figure for the year (as at December 26th). It’s also important to note that I haven’t sold anything so these returns aren’t final. The stock market could drop and all the returns could be wiped out hypothetically next year as I haven’t crystallised these returns. The reason I keep hodling (read: holding) is so that I can benefit from compounding (making returns on the returns I’ve already made) so that my portfolio can grow exponentially in the future. I do not trade (buy and sell assets regularly for short term gains), I do not short (use fancy investment devices to bet on a company failing), I invest (buy into good quality companies/assets that generate strong profits and have decent management teams so I practically become an owner of the company too). Finally, all returns are given as a percentage instead of in nominal terms as I feel it helps give the best understanding that everyone can apply to their own portfolios. Telling you that my portfolio has gone up by a million or down by 50p doesn’t really give you a benchmark that you can apply to your own investments.

What is my investment approach?

I follow a core-satellite approach which means the core of my portfolio is made up of low fee index funds that follow major global markets across a range of asset classes (equities, property, bonds, commodities etc). Then shooting off from that core I have lots of ‘satellites’ – individual assets like specific stocks, cryptocurrencies, whisky and whatever else I find interesting. I use dollar/pound cost averaging to buy into assets gradually with set amounts each month instead of investing a single lump sum.

What is my portfolio structure?

Tax efficiency is important for investing. This is why my investments firstly go into my pension, then a stocks and shares (S&S) ISA. Pension contributions are done before tax and in the UK a S&S ISA can have £20,000 paid into each year without you having to pay any capital gains tax, which is great.

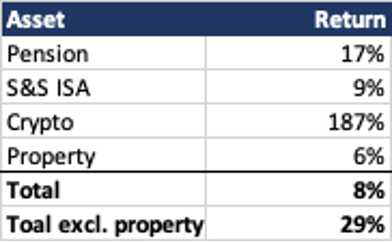

So how much money did I make?

The table below summarises the returns I made on each component of my portfolio:

My pension (core) mainly comprises of low fee index funds and the payment is automated each month along with a top up from my employer. The 17% return shows the power of simply dollar cost averaging into funds each month. The S&S ISA has a range of investments that I have researched and chosen to hold over the long term. I invested a small amount in crypto that I was willing to lose and as you can see it grew a crazy amount over the past year. However, it was a rollercoaster year for cryptocurrencies so I am glad it was an amount I was comfortable with. I also purchased a house at the end of 2020 and it has appreciated in value. I included it to provide a full picture, but because the property value is high compared to the rest of my portfolio it skews results. I decided to include a total return value excluding property because of this reason. So for context, if I had invested £1 I would now have £1.29. If I had invested £1000 I would now have £1290 and if I’d invested £1m I’d now have £1,290,000.

So was this a good year for my investments?

Investors tend to compare their performance against the ‘market’ which is broadly accepted as the S&P 500 which is a benchmark of the 500 largest companies in the USA. The USA is normally used as it makes up such a large percentage of the global stock market. At a very base level I personally don’t think too much about benchmarks – the alternative to not investing is having your money in a bank account losing value as a result of inflation. My main aim is to beat inflation (which is currently around 4% in the UK). However, I do understand that a very easy alternative would be to put all your money into an S&P 500 index fund – which this year has returned about 26%. My overall market investments (excluding my physical property) were up 29% so I more than achieved my goal for this year as well as ‘beating the market’.

What lessons did I learn?

Hindsight is a wonderful thing. Reviewing the breakdown of returns would give you the impression that I should have thrown all my money into crypto! Realistically over the long term a diversified portfolio will not only let you sleep better at night, but will provide decent returns with a level of risk that you can manage appropriately.

As always, let me know if you have any questions in the comments below. Wishing you guys all the best for 2022 and beyond.

Disclaimer: Please remember that none of these blog posts are financial advice and that the value of your investments can go up as well as down.